I never like to talk to insurance agents. The ones who approached me in the past were aggressive to the point of being turn-offs. So it was with a bit of iffy-ness that I attended the “Usap Tayo” meet and greet for bloggers sponsored by Philam Life recently at their Makati building.

What reassured me that this was not the run-of-the-mill spiel to pitch insurance products was the casual invite that just asked “Anong plano mo? Usap tayo!” I was reminded of the “Usap Tayo” TV commercials (TVC) I’d catch during the few times I’d watch TV. These TVCs focused on the lives of those whose future were ensured by insurance proceeds.

|

Larry Cleto, a registered financial consultant (RFC), began with an interesting talk on Financial Planning 101 or How to Save Up for Your Dreams. I have heard talks like these before but when I see the statistics being presented each time, it makes me even more aware that in the Philippines, many people still do not know how to manage their income so that they are able to build up a financial nest to cover their loved ones when disaster strikes.

|

| Larry Cleto |

Here are some things I picked up from Larry:

- An American bank did a survey of how many Filipinos aged 18-40 maintained a bank account. 62% of those surveyed scored <50 out of a perfect 100. The average financial IQ of the Filipino was 48.

- While some Filipinos save, only 1 out of 10 respondents consciously saved for retirement. The others were not sure if it would cover their lifestyle after they retire.

- Only 8% have adequate personal insurance.

- 47% do not know what to do with their savings.

- Wealth management involves 3 goals: Accumulate, Preserve and enjoy it, and Transfer it to your loved ones.

I particularly liked these ideas which Larry Cleto put forth:

1. Financial freedom is the ability to live the lifestyle you desire without having to work or rely on anyone else for money. – Here in the Philippines, many families raise children and expect them to support their parents in their old age. This is something I disagree with. I do not want to put this burden on my kids. We want to provide them with the best education we could afford to give them and with that, we expect them to be able to forge their own future without the obligation of caring for us. For us to successfully carry this out, we ourselves need to be financially independent of our children. It is not right to transfer all our wealth to them. They need to be able to carve their own wealth out for themselves after we have armed them with a good education.

2. Active income and passive income concepts – Active income derives from one’s work. That means then that to have income, one needs to have a livelihood. Passive income is what you get from prudent investing (letting your money work for you and give you ADDITIONAL income). Income from a livelihood is good but must not be the only source for your family because when something happens to you and your livelihood is affected, everyone is affected. This is when passive income comes into play. There should be enough passive income to continue providing for your family even when livelihood income is affected.

3. It is not how much you earn but how much you keep/save that builds wealth – I have heard people say they cannot become rich because they do not earn enough. What will be enough? If one’s spending habits increase as one’s salary increases, there is no way you can accumulate wealth. On the other end of the spectrum, even a janitor or clerk who regularly sets aside a fixed amount from his salary can build this up considerably in as little as 10 years.

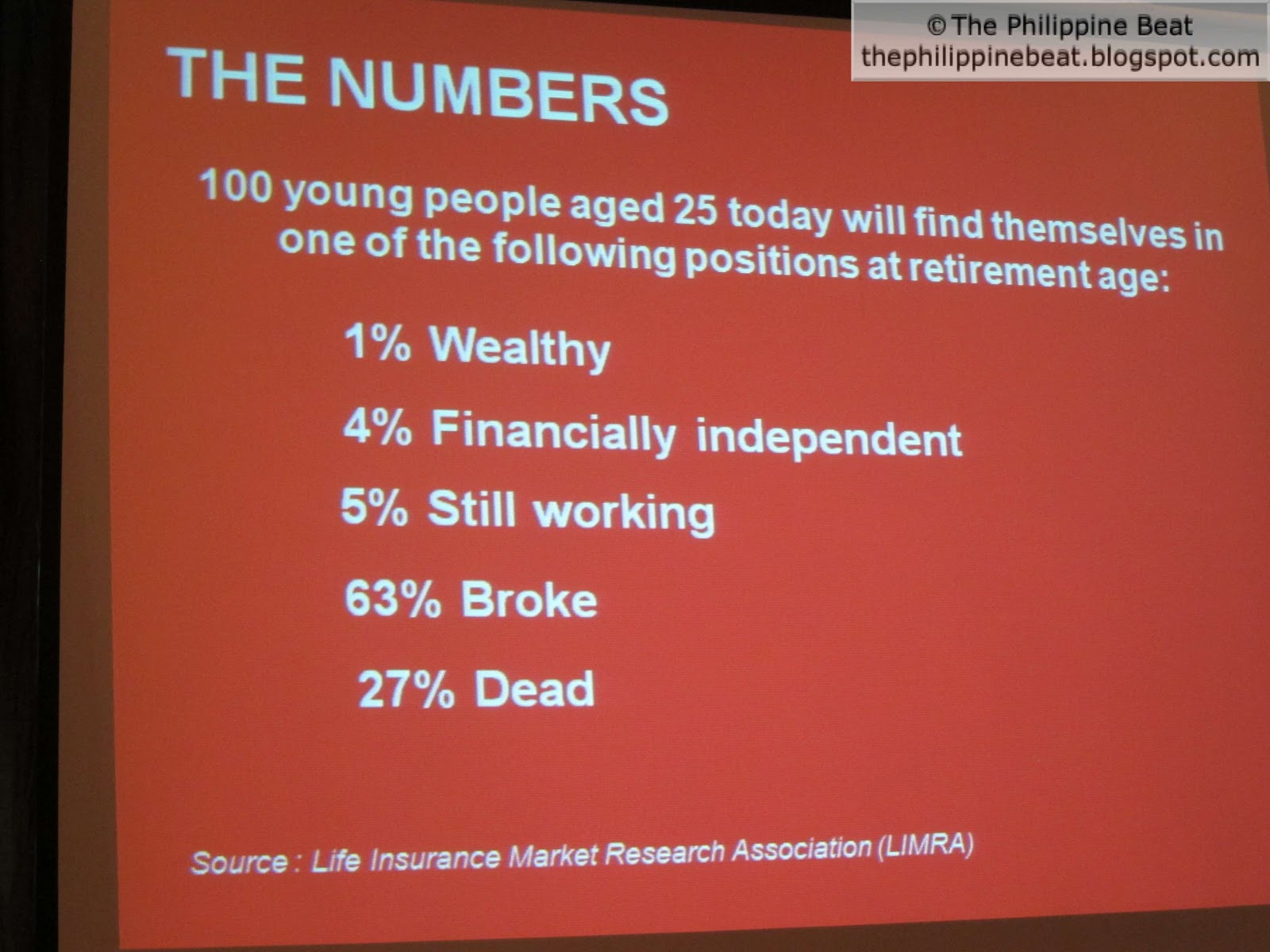

This slide jolted me.

|

| Isn’t it shocking that only 4% would be financially independent when they retire, about 10% would have some form of income, and a shocking 63% will be BROKE??? |

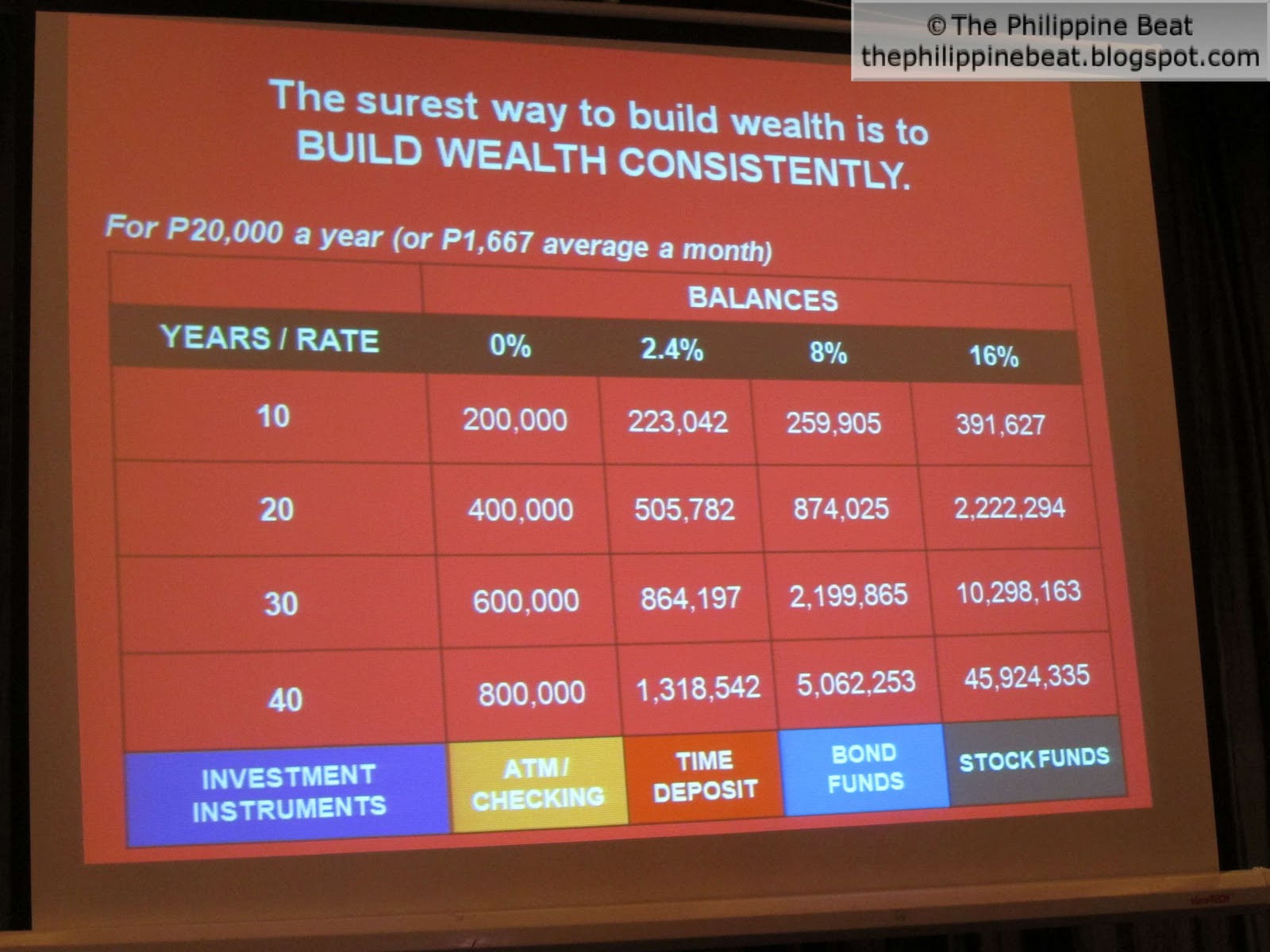

But this slide shows that even saving and wisely investing as low as P1,667 a month can build wealth.

|

| Depending on the investment vehicle you choose, that P1,667 a month can grow to as much as P45 million in 40 years! |

|

| Connie Dizon |

|

| Deorie Caraca and her mom |

This event once again reminded me how important it is for me to continually assess my own family situation. Sometimes we get bogged down with work and busy-ness and put off planning for the future until tragedy stares us in the face and we are caught unprepared.

Do you have your financial life plan clearly mapped out already?

If the answer is NO, today is the best time to begin planning one. Financial literacy is not only for business majors or for those schooled in finance. Each one of us needs to have some level of literacy to be able to prudently invest our hard-earned money so that it works for us down the road.

Philam Life maintains its corporate website HERE and the “Usap Tayo” site HERE. Or call telephone (02) 528-2000 to talk to a Philam Life financial planner.