Do you wonder if an 8 to 5 job is really for you?

Do you have young kids and you wish you had more time with them?

Do you wish you could earn more than your current salary?

Do you love traveling but you know it takes a lot of money to do so?

If you answered YES to any of those questions, read on because this may be an alternative career path for you.

Quick Flashback…

I quit cold turkey from a job as Vice President of a bank, with a fairly promising career path, in order to be a full-time Mom to four kids. It took a while to make the decision, primarily because I was a very driven corporate person, had never been jobless since I graduated, and I knew going back to a single income would make a dent in the family’s income stream. But I knew inside me that I did not want a job that kept me till weekends and late nights at the office while my kids were raised by yayas. I wanted to be present to them.

Some female colleagues in the bank who heard I was quitting actually wished they had my kind of option. Many of them had to work to augment the family income. It was sheer prudent spending and tight budgeting that got me through all those years without a job.

Thankfully, the internet and technology have now developed to the point where a new direction has opened up for people like me – telecommuting work. I am kept busy by blogging, article writing, advocacies and all these while being able to stay home most days, visible to my kids.

But are there options other than telecommuting work?

Of course. One can get into entrepreneurial ventures, join multilevel marketing companies, and other business endeavors but often, these do take a lot out of you at the onset due to startup pains.

There is another way that is less painful.

Several of my lady blogger friends and I met up over lunch with Christine Lee and Dar Uyco from Sun Life Financial, so they could present opportunities for you if you wish to consider becoming a Sun Life Financial Advisor.

If any of you are cringing right now, you are probably thinking this post is for someone who will be hard-selling insurance just like those who approach you in malls, go door to door, or aggressively call you up to ask to make a presentation. Before coming to this meeting, I asked precisely about this because the last thing I wanted to do was to attend a meeting where I’d be invited to be some kind of insurance agent or ‘ahente’. I personally avoid hard-selling agents and one of my pet peeves is to be accosted at a mall and be offered some kind of product.

I was assured this wasn’t the case.

Financial Advisor vs The ‘Ahente’

Thankfully, this was the first apprehension tackled by the Sun Life Financial team when we met up. The ‘ahente’ stereotype is what Sun Life wants to redefine and differentiate. With the backing of a large insurance company, they want to equip their financial advisors with professional skills — not simply selling skills — to read into the situation of each and every potential individual or company they are approaching in order to offer a product which comes close to, if not exactly to, what the client needs.

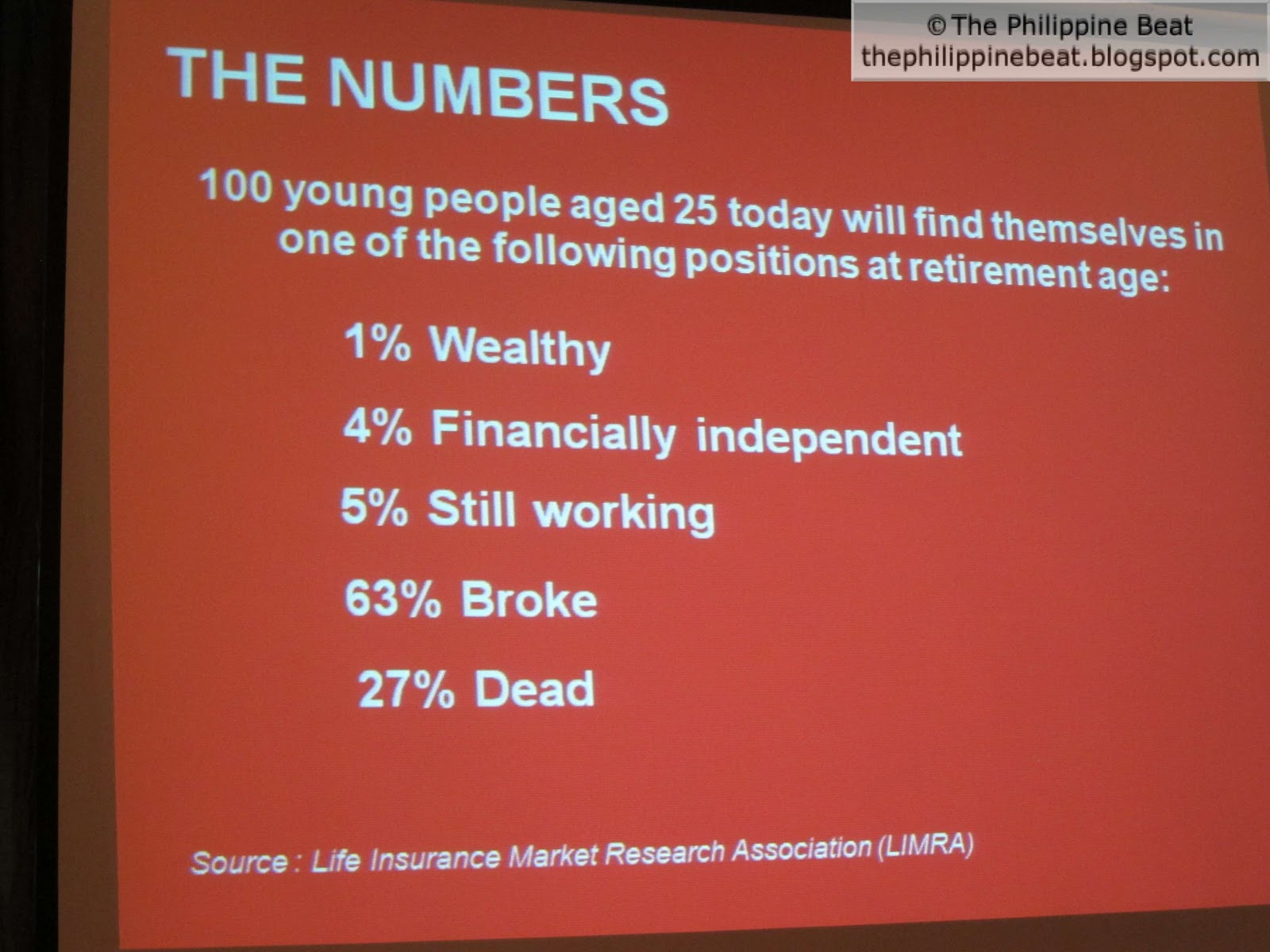

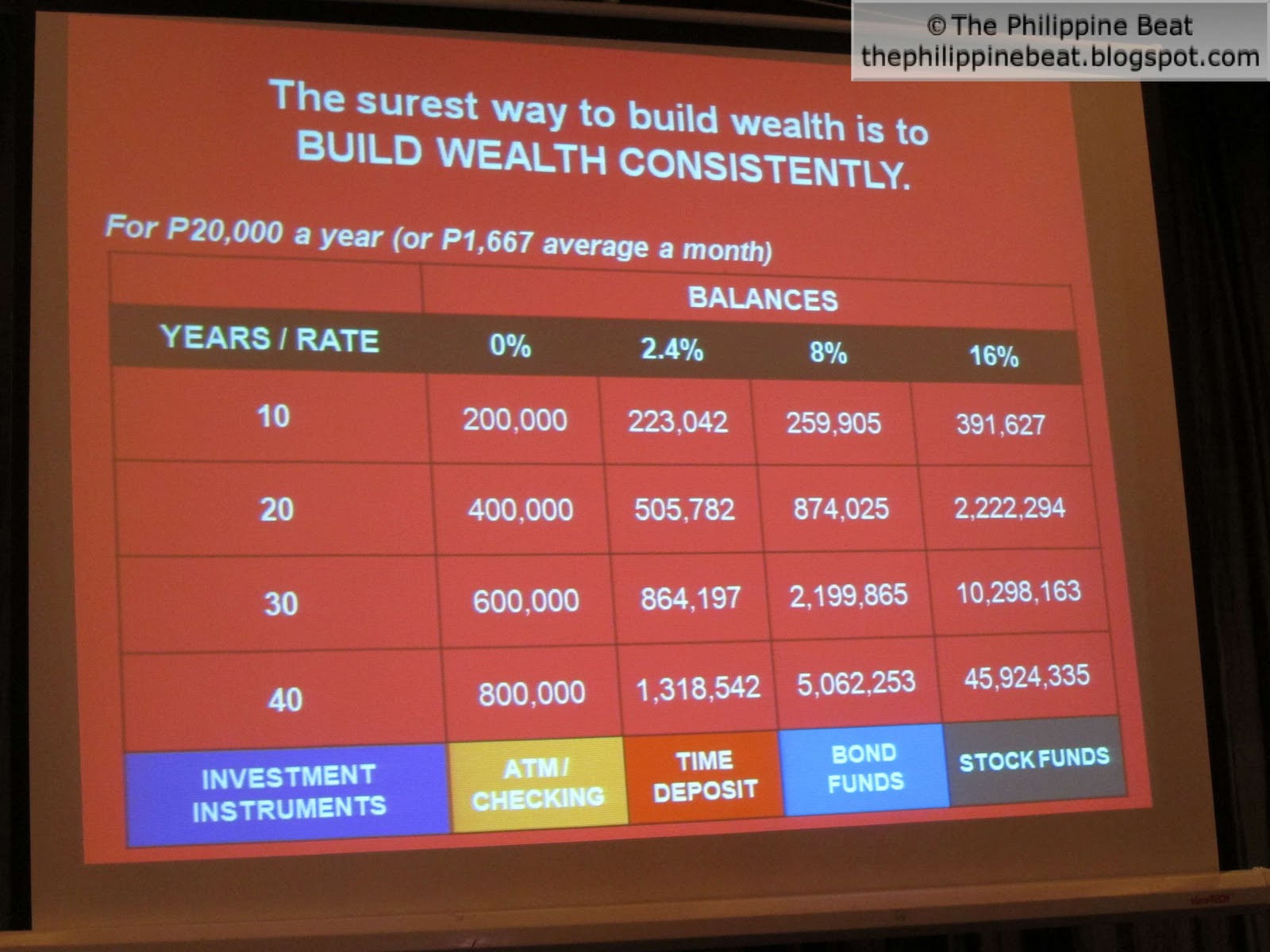

With interest rates so painfully low, simply parking money in savings or even time deposit is no longer an investment option. Inflation will easily eat up the interest gains in those products. If one is planning to build a financial nest large enough to sustain him into his senior years, then more strategic and well-placed investment choices need to be made early on.

The role of a financial advisor is important in identifying the long-term financial goals of each individual and recommending the appropriate insurance product that one can ably pay for during earning times and which will cover him/her when capacity to earn is diminished or lost. In a way, I think it is fulfilling to be in the shoes of a financial advisor because you are not earning just for yourself and your family but you are ensuring that someone else’s future is also secured.

What Sun Life Financial is offering someone interested in becoming a financial advisor (FA) are the following:

1. Monthly Kapihan sessions – give current market updates and trends to look out for;

2. Leadership programs for its Management team as opposed to Management programs. Why? Because one can have the title ‘Manager’ and yet, lack leadership skills.

3. Collaboration with the Asian Institute of Management (AIM) to create the 1st Certified Financial Planning Course (CFP) in the Insurance Industry. This program already produced 27 graduates. It will be cascaded down to its FA’s in the next 3-5 years.

Dar and Christine related how they actually never contemplated working in the insurance industry but their separate circumstances eventually led them to Sun Life Financial. They were part of the first batch that finished the CFP course in AIM. And the financial rewards that came with their efforts were more than they initially expected. Through Sun Life, they were also able to travel to foreign places that are not normally the run-of-the-mill tourist places but exotic, educational ones (think Russia, for example).

But just so reality sets in, here’s a table showing the pros and cons of this kind of work:

I think the major CON for many looking for something stable is the lack of a fixed monthly compensation. The salary scheme is purely commission-based. But, if one has the business aptitude, positive attitude, right network and hardworking, the financial rewards can actually significantly exceed a regular monthly salary.

For starters, this is a brief of the type of people they are looking for:

Male or Female, 21-35 years of age

College Graduate

Filipino/Foreigners with ACR/ICR

Driven to Succeed

Sales background not necessary

High Integrity

People Person

Financial Background a plus, but not necessary

If you are beyond the age mentioned above, no worries. Just give them a call to see if you can still apply. Not sure if your educational background is sufficient to make you a financial advisor? They do say it is a plus to have some financial background but their training programs pretty much prepare one who doesn’t have it.

Sometimes, you never know if you have it in you. Many of those with Sun Life Financial now never planned to join but somehow found their way to it and now attest to its being fulfilling and financially rewarding.

If you are in between jobs, have been a stay-at-home parent or still employed but looking for more flexi options, could this be an option for you?

Contact: Darwin Uyco, Unit Manager

Tel: (02) 719-3815

Mobile: +63917 8988926

Email: darwin.d.uyco@sunlife.com.ph

Sun Life Financial – Red Spruce Unit

G/F E-Square Building

Ortigas Ave., Greenhills

San Juan, Metro Manila